Selamat Datang di LPPI Jakarta

HIGHLIGHTS (Klik untuk info selengkapnya)

VIRTUAL SEMINAR & PODCAST LPPI

|

|

VENUE LPPI

LIPUTAN KEGIATAN

19

Mar

Penandatanganan Perjanjian Kerja Sama LPPI dengan Institut Teknologi dan Bisnis Ahmad Dahlan

"Jakarta, (15/03) LPPI dan Institut Teknologi & Bisnis Ahmad Dahlan (ITB AD) bersatu dalam semangat kolaborasi untuk meningkatkan kompetensi sumber daya manusia di sektor perbankan. Dengan penandatanganan Perjanjian Kerja Sama, mereka resmi memulai Program ToT Beyond Excellent Trainers yang diawali ... (Selengkapnya)

08

Mar

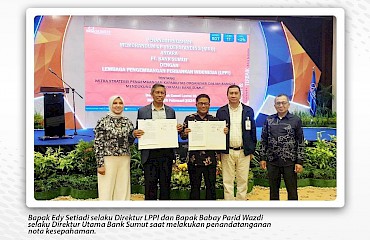

LPPI dan Bank Sumut Menandatangani Memorandum of Understanding (MoU)

LPPI dan Bank Sumut menandatangani Memorandum of Understanding (MoU) dalam rangka pengembangan kapabilitas organisasi dan mendukung program tansformasi agar dapat bersaing di wilayah Sumatera Utara dan Nasional. ... (Selengkapnya)

08

Mar

Program Pemimpin Cabang Angkatan 202 Melakukan Benchmarking ke Tokyo

Program Pemimpin Cabang Angkatan 202 melakukan benchmarking ke Tokyo dan kunjungi BNI dan KBRI Tokyo. Benchmarking ini didampingi langsung oleh Direktur LPPI, Ibu Retno W. Wijayanti. ... (Selengkapnya)

PROGRAM PELATIHAN

25

Mar

Program ToT Beyond Excellent Trainers: Guiding Future Professional Banker

LPPI bekerja sama dengan ITB Ahmad Dahlan dalam pelaksanaan program "ToT Beyond Excellent Trainers: Guiding Future Professional Banker" yang diikuti oleh 16 peserta yang merupakan dosen hingga petinggi ITB Ahmad Dahlan. Program ini merupakan agenda lanjutan setelah sebelumnya pada 15 Maret 2024, ... (Selengkapnya)

13

Mar

Penutupan Program Pemimpin Cabang Angkatan 202

LPPI sukses menyelenggarakan Penutupan Program Pemimpin Cabang Angkatan 202.

Pada kesempatan ini, Direktur LPPI Ibu Retno W. Wijayanti hadir untuk memberikan sambutan sekaligus menutup program tersebut. Program Pincab kali ini diikuti oleh sebanyak 23 peserta yang terdiri dari Bank BPD di seluruh ... (Selengkapnya)

29

Feb

Pelatihan Manager-Supervisor Development Program (MSDP) Batch ke-2 Bank NTB Syariah.

LPPI terus mengembangkan kompetensi Sumber Daya Manusia (SDM) industri keuangan dengan melaksanakan pelatihan Manager-Supervisor Development Program (MSDP) Batch ke-2 Bank NTB Syariah. ... (Selengkapnya)

Otoritas

![]()

![]()

![]()

![]()

Copyright ©2024. Lembaga Pengembangan Perbankan Indonesia